Quick liquidity despite poor credit rating: what options are available to drivers?

When neither traditional sales nor a loan are possible

An unexpected tax bill, a major repair or a short-term liquidity bottleneck: unplanned expenses rarely come in handy. It becomes particularly difficult when the bank rejects a loan application in such cases. A negative extract from the debt enforcement register or a poor credit rating are often enough for traditional credit solutions to be cancelled. Car drivers in particular are then faced with a dilemma: money is needed - but so is the vehicle. What options are there in Switzerland if a regular bank loan is not an option?

Why a bank loan is often not an option

In Switzerland, banks systematically check the creditworthiness of every loan application - they have to, for legal reasons there is no way around it. The extract from the debt collection register plays just as central a role as the information originating from credit and credit agencies . Even single entries can lead to rejection.

So if you are looking for a credit alternative without a debt collection register extract, you will quickly realise that the range of products on offer is limited and many of those advertised online as "credit without a credit check" are of dubious reliability.

In addition, consumer loans are subject to strict legal requirements. Lending "without a credit check" is therefore de facto not possible in the traditional sense.

The reality:

Traditional bank loans are practically impossible with a negative credit rating - legal requirements do not allow any exceptions in this regard.

Selling your car? Not a real solution for many

A roadworthy vehicle always represents a certain value - and itself incurs avoidable costs. Selling it is therefore an obvious idea, but one that often fails to materialise in everyday life:

This is why many people specifically look for a car pawnshop or a car pawnshop - in the hope of using the vehicle as collateral and still being able to continue driving.

Car pawnshops in Switzerland: what is realistic?

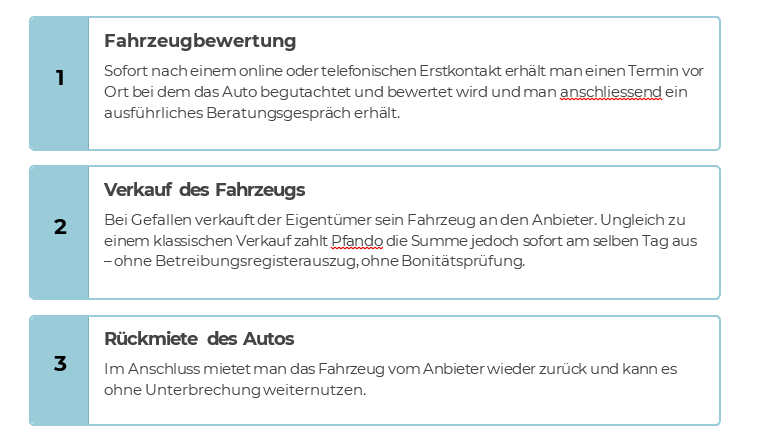

The classic model of a car pawnshop is simple:

The biggest problem with this: In Switzerland, this model is hardly widespread for private individuals. Pawnbroking is subject to cantonal authorisation and is highly regulated. In addition, the vehicle usually remains with the provider in a classic pawn transaction. This means that as long as the claim is outstanding, the car cannot be used - similar to a sale.

For many, this is precisely the crucial catch. Those who need short-term liquidity usually still need mobility.

For some time now, a different model has therefore been established in Switzerland, which is often colloquially referred to as a car pawnshop, but works differently in legal terms: The so-called sale and rent back - decisive grossgemacht from the Provider Pfando.

The principle is comparatively simple:

As this is not a classic pawn shop, but a car pawnshop alternative that works differently, the classic car pawnshop rules do not apply - and neither do those of classic loans. The car remains with the previous user. It is not stored, but remains usable in everyday life.

Sale and Rent back is therefore often perceived as a credit alternative without a debt collection register extract.

The reason is obvious: it is not a loan in the traditional sense, but a sales transaction with a rental agreement. As no loan is granted, no credit check is required. This model can therefore be a realistic option for people with limited creditworthiness - especially if the vehicle is owned by the customer and can therefore be sold without any problems.

For whom is such a car pawnshop alternative suitable?

Sale and Rent back as a modern, customer-friendly alternative model to the car pawnshop can be particularly suitable for

- Persons with a negative debt collection register extract

- People with a poor credit agency score

- Self-employed persons with fluctuating income

- Persons with short-term liquidity requirements (e.g. tax receivables, insurance premiums, repairs...)

- Situations in which mobility must be maintained

However, the model is less suitable when...

- the vehicle is to be sold permanently anyway

- the monthly rental costs are not sustainable in the long term

- the car legally belongs to a third party - for example in leasing constellations

Like any financial solution, this option is not a panacea, but an instrument for certain situations - where the credit alternative without a debt collection register extract can often be the best and sometimes the only solution.